Chargebacks are one of the most underestimated threats to a prop firm’s financial stability. A single wave of disputes can freeze your payment processing, wipe out weeks of revenue, and in extreme cases, get your merchant account terminated entirely.

Most content on this topic is written for traders explaining how to dispute a charge. This guide is written for operators — the people on the other side of that dispute, trying to run a sustainable business.

Why Prop Firms Are Particularly Vulnerable

Prop firms sit in a uniquely exposed position when it comes to chargebacks. Here’s why:

High-risk merchant category. Payment processors classify prop firms as high-risk merchants. This means your chargeback threshold is lower than a typical e-commerce business — in many cases, exceeding 1% chargeback ratio triggers penalties, account review, or termination.

Digital products with no physical delivery. Challenge fees are digital transactions. There’s no shipping confirmation, no physical product, no delivery proof. This makes it easier for traders to dispute charges and harder for you to win representment cases without solid documentation.

Emotionally motivated disputes. Traders who fail a challenge, get their funded account closed for a rule breach, or simply feel the rules were unfair are motivated to file chargebacks. Unlike a confused customer who forgot a subscription charge, these are deliberate disputes — often filed with a narrative already constructed.

High transaction volume. A growing prop firm processes hundreds or thousands of challenge fee transactions monthly. Even a 2-3% dispute rate creates a meaningful operational and financial burden.

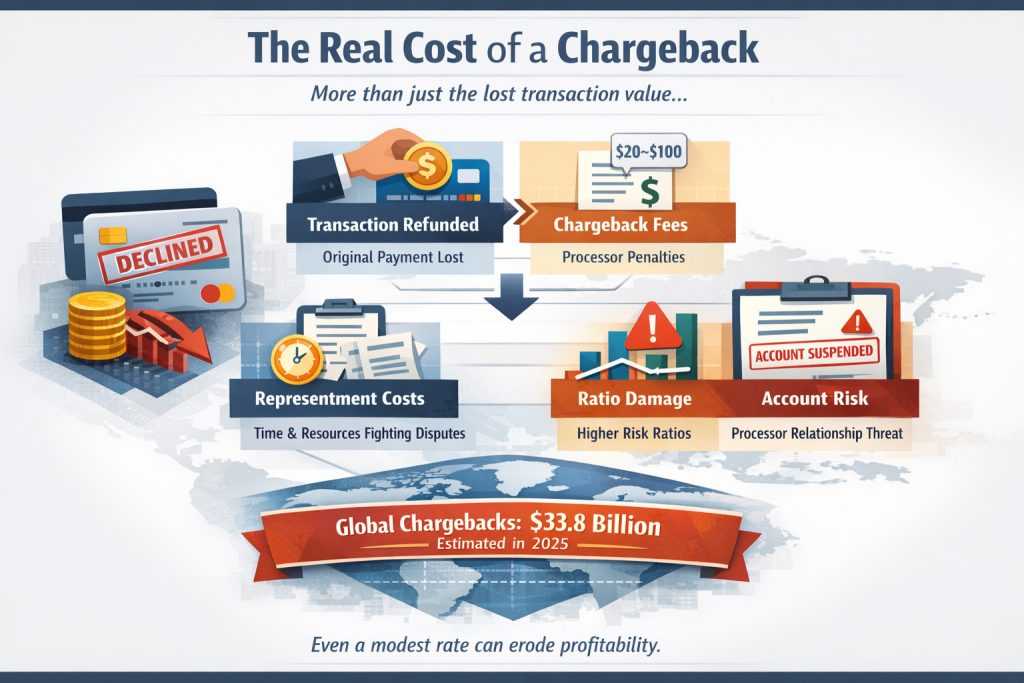

The Real Cost of a Chargeback

Most operators focus on the lost transaction value. That’s only part of the picture.

Each chargeback typically costs you:

- The original transaction amount — returned to the cardholder

- Chargeback fee — typically $20–$100 per dispute charged by your payment processor

- Representment costs — time and resources to fight the dispute

- Ratio damage — even won chargebacks count toward your ratio in many schemes

- Processor relationship risk — sustained high ratios can get your account flagged, placed in monitoring programs, or terminated

Global chargebacks cost merchants an estimated $33.8 billion in 2025. For prop firms operating on tight margins between challenge revenue and trader payouts, even a modest chargeback rate can meaningfully erode profitability.

Where Chargebacks Come From in Prop Firms

Understanding the source helps you target the right prevention measures.

1. Friendly fraud after a failed challenge The most common scenario. A trader fails phase one or two, decides the challenge was unfair, and disputes the fee with their bank claiming the service wasn’t delivered. Often framed as “I didn’t receive what was promised.”

2. Post-breach chargebacks on funded accounts A trader gets funded, violates a rule, loses their account, then disputes all their previous challenge fees simultaneously. This pattern — multiple chargebacks from a single trader — is particularly damaging.

3. Genuine billing confusion Some disputes come from traders who don’t recognize the charge on their statement, or whose family member made the purchase without their knowledge. These are recoverable with good documentation.

4. Fraud A smaller but growing segment involves traders using stolen payment details to purchase challenges. When the real cardholder notices, they dispute. You lose the challenge fee and potentially the funded account exposure.

5. Escalated complaints Traders who can’t get a response from your support team, or feel their complaint has been ignored, sometimes turn to chargebacks as a last resort. These are often preventable with better customer service infrastructure.

Prevention: The First Line of Defense

The most effective chargeback strategy is preventing disputes from being filed in the first place.

Crystal clear terms and conditions Your terms need to explicitly state that challenge fees are non-refundable once platform access is granted. Include what constitutes a rule breach, what triggers account termination, and what the dispute process is. Vague terms are your enemy — every ambiguity becomes a trader’s argument.

Transparent rule enforcement A trader who understands exactly why their account was closed is far less likely to dispute than one who receives a generic “your account has been terminated” message. Your prop firm CRM and back office should generate detailed breach notifications with timestamps, specific rule violations, and supporting data automatically.

Confirmed acceptance at checkout Implement mandatory checkbox confirmation at purchase: “I confirm I have read and agree to the terms and conditions, including the no-refund policy.” Log this confirmation with a timestamp. This single step significantly strengthens your position in representment.

3D Secure authentication Enabling 3DS2 at checkout provides a liability shift — if a transaction is authenticated and later disputed as unauthorized, the liability moves to the issuing bank, not you. For high-value challenge purchases, this is essential.

Recognizable payment descriptor Make sure your company name appears clearly on card statements. A significant portion of “friendly fraud” chargebacks start as genuine confusion — the trader doesn’t recognize the charge. A clear descriptor prevents this.

Documentation: Your Evidence Package

When a chargeback is filed, you have a window — typically 7 to 20 days depending on the card network — to submit a representment package. The quality of your evidence determines whether you win or lose.

What to include:

- Transaction record — date, amount, payment method, IP address

- Terms acceptance log — timestamp showing the trader accepted your terms at checkout

- Platform access log — proof that the trader logged in and used the platform after purchase

- KYC documentation — verified identity linking the cardholder to the account

- Communication history — all emails, support tickets, and chat logs with the trader

- Rule breach evidence — if the dispute follows an account closure, include the specific breach data with timestamps

- Challenge activity log — trades placed, dates, performance data showing the platform was actively used

This is where your back office and reporting infrastructure becomes critical. If you can’t pull a complete activity log for any account within minutes, you’re going to lose representment cases you should win.

Operational Practices That Reduce Chargeback Risk

Beyond payment-level controls, how you run your operation day-to-day has a significant impact on your chargeback rate.

Respond to support tickets fast A large proportion of chargebacks from genuinely dissatisfied traders are filed because they couldn’t get a response from support. A ticket that sits unanswered for 5 days becomes a chargeback. Set response time SLAs and enforce them.

Communicate rule breaches proactively When an account is closed for a rule breach, send an immediate, detailed notification. Include what rule was violated, when it happened, and what the data shows. Give the trader a clear internal dispute process before they go to their bank.

Offer an internal dispute process Having a formal internal appeals process — where traders can contest a decision before filing a chargeback — diverts disputes away from the payment system. Many traders will use it if it exists and feels fair. This is also good for prop firm reputation management — it signals that you’re willing to engage rather than ignore.

Flag high-risk accounts early Some traders show behavioral signals that correlate with chargeback risk — multiple failed challenges, aggressive support contacts, complaints on social media. Your CRM should flag these accounts so your team can pay closer attention and ensure documentation is complete before any account action is taken.

Managing Your Chargeback Ratio

Your chargeback ratio is the percentage of transactions that result in disputes within a given month. Staying below the thresholds set by card networks is essential to maintaining your merchant account.

Visa threshold: 0.9% (standard) / 1.8% (excessive) Mastercard threshold: 1.5%

Exceeding these thresholds places you in monitoring programs — Visa’s VDMP or Mastercard’s VAMP — which come with monthly fees and requirements to reduce your ratio within a set timeframe. Continued non-compliance results in account termination.

Track your ratio monthly. If it starts climbing, investigate the source immediately rather than waiting for it to become a processor problem.

Payment Processing Strategy for Prop Firms

Because prop firms are high-risk merchants, your payment processing setup needs to be more sophisticated than a standard business.

Work with PSPs that understand prop firms Not all payment service providers will work with prop firms, and those that do have varying levels of understanding of the business model. A PSP with experience in the prop trading space will have better guidance on chargeback prevention and more tolerance for the dispute patterns typical in the industry. Choosing the right payment solution from the start saves significant operational pain later.

Diversify your payment methods Relying on a single payment processor creates existential risk. If that processor suspends your account due to chargeback ratios, your entire revenue stream stops. Maintain relationships with multiple processors and offer alternative payment methods — crypto, bank transfer, alternative PSPs — that reduce your credit card chargeback exposure.

Reserve funds Many high-risk processors hold a rolling reserve — typically 5-10% of monthly processing volume — as protection against chargebacks. Factor this into your cash flow planning.

What to Do When Chargebacks Spike

If your chargeback rate suddenly increases, treat it as an operational emergency.

- Identify the source — Are disputes clustering around a specific challenge product, a specific time period, or a specific group of traders? The pattern tells you what’s driving it.

- Review your terms and communications — Did something change in your rules or enforcement that traders are reacting to?

- Audit your support response times — Are tickets being left unanswered?

- Contact your processor proactively — Don’t wait for them to contact you. Proactive communication about a spike and your mitigation plan is viewed far more favorably than silence.

- Submit representment on every disputable case — During a spike, fight everything you can win. Recovery rate matters for your ratio.

Bottom Line

Chargebacks are an operational reality for prop firm operators, not an edge case. The firms that manage this well treat it as a systems problem — building the right documentation infrastructure, the right payment setup, and the right internal processes before disputes become a crisis.

The firms that get caught off guard are usually the ones that grew quickly without putting these systems in place. By the time chargebacks become a problem, they’re already affecting processor relationships and cash flow.

Prevention is cheaper than recovery. And recovery is possible — but only if you have the evidence to fight.

Request a Consultation on Chargeback Risk Strategy for Prop Firms

Get expert guidance on structuring your prop firm’s payment and dispute framework to minimize chargeback exposure. We’ll help you evaluate merchant setup, documentation standards, rule enforcement transparency, and operational workflows before disputes escalate into processor risk.

Together, we’ll review your current chargeback profile and outline a structured prevention strategy aligned with sustainable growth.