Payment infrastructure is one of the most operationally complex layers of a forex brokerage or prop firm. Unlike standard e-commerce payments, forex and prop firm transactions must integrate with KYC status, trading account balances, internal ledgers, risk monitoring, and compliance workflows simultaneously. Getting this infrastructure right determines how fast traders can fund, how reliably they can withdraw, and how well the brokerage manages chargeback exposure and regulatory audit requirements.

This guide covers the main funding methods used by forex brokers, how PSP aggregators work, the role of crypto payments, and what to evaluate when selecting and integrating payment providers. For the product overview, visit the Forex Payment Solutions page.

Why Forex Payments Are Different From Standard Payment Processing

General-purpose payment providers are designed for e-commerce: a customer pays, the merchant receives funds, the transaction is complete. Forex and prop firm payment flows are structurally different at every step.

Traders expect deposits to be credited to their trading account immediately or within minutes — not after a manual review cycle. Withdrawals need to be processed to the same method used for the deposit in most regulated jurisdictions. KYC status must be verified before the first withdrawal is approved. Chargebacks on challenge fees are a primary operational risk for prop firms and need active dispute management. And every transaction needs to be visible in the CRM with a full audit trail connecting the payment event to the client account, KYC record, and trading platform balance.

General PSPs rarely provide the trading-platform workflow logic that brokers and prop firms need. This is why payment integration for forex is a specialized function, not a standard checkout implementation.

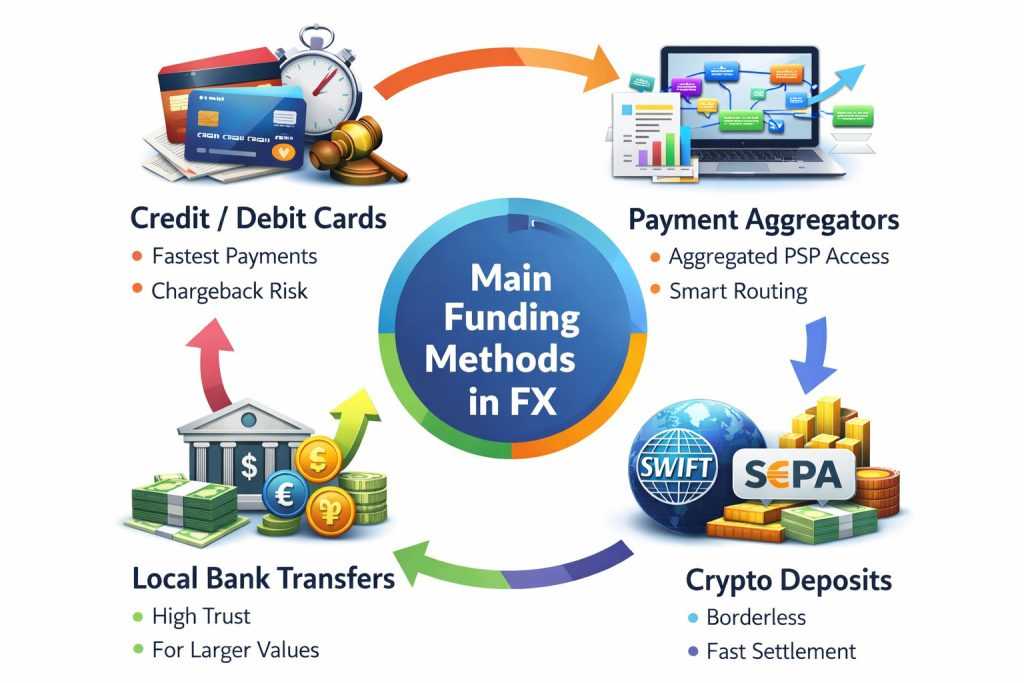

Main Funding Methods in Forex

Each funding method has different characteristics in terms of speed, geographic coverage, chargeback risk, and operational complexity. Most brokers and prop firms support multiple methods to serve different trader segments and regions.

Credit and Debit Cards

Cards remain the most common deposit method for retail forex and prop firm clients — fast crediting, familiar to traders, and available in most markets. The operational challenge is chargeback risk. Forex and prop firm merchants are classified as high-risk by card networks, resulting in higher processing fees and stricter chargeback thresholds. For prop firms, challenge fee chargebacks are a significant revenue risk — a trader who fails a challenge and disputes the fee creates both a financial and operational burden.

Effective card payment management requires robust dispute handling, velocity rules that flag suspicious deposit patterns, and clear terms and conditions that strengthen the merchant’s position in chargeback disputes.

PSP Aggregators

A PSP aggregator connects multiple payment providers through a single interface. Rather than integrating each PSP independently, the broker connects to the aggregator and gains access to multiple providers simultaneously — with intelligent routing logic that selects the optimal processor for each transaction based on geography, card type, and approval rate history.

For forex brokers, aggregator logic needs to go beyond standard routing. It should connect deposit confirmation to KYC tier verification, link funded amounts to trading account balances, enforce transaction limits based on client risk profile, and generate reconciliation reports that the finance and compliance teams can use directly. Aggregators that understand the forex vertical build this logic in. General aggregators require custom development to achieve the same result.

Bank Transfers and Local Payment Rails

Bank transfers remain essential for regulated brokers, high-value clients, and regions where card acceptance rates are low. They carry lower chargeback risk than cards and are the preferred method for larger withdrawal amounts in most regulated jurisdictions.

Local payment rails — PIX in Brazil, ACH in the US, SEPA Instant in the EU, UPI in India — significantly improve approval rates and processing speed compared to international wire transfers. For brokers targeting specific regional markets, supporting the local rail is often the difference between competitive and uncompetitive funding experience for traders in that region.

Crypto Deposits and Withdrawals

Crypto has become a major funding channel for global brokers and prop firms, particularly for markets where traditional banking infrastructure creates friction — parts of Asia, Africa, the Middle East, and Latin America. Settlement is fast, geographic restrictions are minimal, and stablecoins like USDT eliminate the volatility risk of holding BTC or ETH in the payment flow.

Operational requirements for crypto payments include AML and KYT (Know Your Transaction) screening on wallet addresses before crediting balances, defined confirmation thresholds before funds are released, conversion partners for stablecoin-to-fiat conversion, and treasury procedures for managing crypto holdings. In 2026, regulators in the EU (MiCA framework) and other jurisdictions are applying formal requirements to crypto payment flows that previously operated without regulatory oversight — brokers accepting crypto need compliance infrastructure that reflects these updated requirements.

How the Deposit Verification Flow Works

A well-structured deposit flow in a forex brokerage or prop firm CRM runs as follows:

- Client initiates a deposit in the Trader’s Room or client portal

- KYC status and account eligibility are verified against the CRM record

- Transaction is routed to the appropriate PSP or payment rail based on method, geography, and routing rules

- Automated or manual confirmation logic verifies the transaction and applies risk checks

- Balance is credited to the trading platform wallet or account and the CRM ledger is updated

Some brokers configure instant balance credit for trusted PSPs with low chargeback history. Others use a verify-and-release flow that holds funds for a short review period before crediting. The right approach depends on the broker’s risk profile, trader segment, and compliance requirements.

Payment Infrastructure for Prop Firms

Prop firms have specific payment requirements that differ from standard forex brokers. Challenge fee collection, funded trader profit distributions, and affiliate commission payouts all need to run through the same infrastructure with different logic for each flow.

Challenge fee collection is a high-volume, relatively low-value transaction type — similar to subscription or digital goods payments. The primary risk is chargebacks from traders who fail challenges and dispute the fee. Effective chargeback management requires clear terms that establish the non-refundable nature of evaluation fees, automated dispute evidence generation, and velocity monitoring that flags traders who make multiple purchases followed by disputes.

Funded trader profit distributions involve larger transaction values and require KYC verification before the first payout is processed. In 2026, PSPs and acquiring banks require documented KYC for all funded trader payouts — prop firms that process payouts without verified identity documentation face merchant account risk. The Prop Firm Payment Solutions infrastructure connects KYC verification directly to payout approval logic, holding distributions in pending status until verification is complete.

Selecting a Payment Provider — What to Evaluate

Not all payment providers support the forex and prop firm vertical. Those that do vary significantly in their coverage, risk appetite, and technical capability. Key evaluation criteria:

- Vertical licensing — explicit support for FX and CFD merchants, not just general financial services

- Chargeback tooling — velocity rules, fraud models, dispute evidence automation

- Fee structure — processing fees, FX spread on currency conversion, settlement fees, monthly minimums

- Settlement terms — timing, supported currencies, reconciliation file format

- Technical integration — API documentation quality, webhook reliability, routing rule flexibility, uptime history

- Compliance support — KYC/AML integration, crypto AML/KYT capability, audit log export

- Support SLAs — merchant support response times, incident communication procedures

Providers that perform well on most of these criteria for general merchants sometimes underperform specifically for forex due to the chargeback profile and regulatory complexity of the vertical. Evaluating against forex-specific criteria — not general e-commerce criteria — produces better selection decisions.

Automation — Reducing Manual Payment Operations

Manual payment operations do not scale. A brokerage processing hundreds of deposits and withdrawals daily cannot maintain a manual review step for each transaction without significant operations overhead and client experience degradation. Payment automation in the CRM covers:

- Automatic deposit confirmation by method, amount threshold, or KYC tier

- Trading platform wallet synchronization on deposit confirmation

- Crypto confirmation tier logic — release funds after defined block confirmations

- Suspicious pattern monitoring and alert routing to compliance team

- Unified settlement reports for finance and compliance across all payment methods

Conclusion

Payment infrastructure is not a commodity decision for forex brokers and prop firms. The funding methods, routing logic, compliance integration, and automation layer all need to be designed specifically for the operational requirements of the financial services vertical — and they need to connect to the CRM, trading platform, and compliance systems that the brokerage runs on.

Kenmore Design’s payment infrastructure connects card PSPs, aggregators, bank rails, and crypto settlement systems to KYC verification, risk logic, and trading platform balances — providing a brokerage-grade payment workflow rather than a generic payment integration. For a full overview of available integrations and configuration options, visit the Forex Payment Solutions page or schedule a demo.

Request a Consultation on Designing a Forex Payment Infrastructure

Get expert guidance on structuring a reliable and compliant payment stack for your forex brokerage. We’ll help you evaluate PSPs, aggregators, bank rails, and crypto funding options — ensuring they align with your regions, risk profile, and operational goals.

Together, we’ll review your business model and outline a payment strategy that supports fast funding, smooth payouts, and long-term scalability.