The foreign exchange market is the largest and most liquid financial market in the world, with daily trading volume reaching $9.6 trillion in April 2025 according to the Bank of International Settlements — a 28% increase from $7.5 trillion just three years earlier. Yet most people who interact with it see only a small slice: a trading platform, a broker, a price feed. The infrastructure behind that experience involves a layered ecosystem of participants, each playing a distinct role in how exchange rates form, how orders get executed, and how liquidity reaches the OTC forex market.

Understanding who these participants are — and how they interact — is essential context for anyone building or operating a forex business. Unlike an equity exchange with a central venue and a single clearing price, the forex market is decentralised and fragmented across dozens of venues and liquidity pools. The mid-market rate a trader sees is the product of relationships and market infrastructure that most participants never directly observe. A clear explanation of how this structure is organised — and who sits at the top of it — is worth reading before going deeper into the individual participant categories.

Quick Overview: Forex Market Participants at a Glance

| Participant | Primary Role | Market Access |

|---|---|---|

| Central Banks | Monetary policy, direct intervention | Direct |

| Tier 1 Banks | Interbank trading, price discovery | Direct |

| Sovereign Wealth Funds | Cross-border investment, portfolio rebalancing | Via prime brokers |

| Prime Brokers | Credit, liquidity access, clearing | Direct |

| Electronic Liquidity Providers | Algorithmic market making | Direct |

| Liquidity Aggregators | Price consolidation, smart order routing | Via prime brokers |

| Hedge Funds | Speculative trading, carry trades | Via prime brokers |

| Retail Forex Brokers | Market access for retail clients | Via Prime of Prime |

| Multinational Corporations | Currency hedging, trade settlement | Via banks/brokers |

| Retail Traders | Speculation, hedging | Via retail brokers |

| Regulators | Rule-setting, oversight | N/A |

1. Central Banks and Monetary Authorities

Central banks and monetary authorities sit at the apex of the forex market hierarchy. They are not commercial market makers — they don’t continuously quote bid and ask prices to retail participants — but their monetary policy decisions define the macro environment in which all other participants operate.

How Central Banks Influence the Forex Market

- Interest rate decisions — adjusting rates changes the relative yield on holding a currency, triggering capital flows that move exchange rates over days, weeks, and months

- Direct intervention — buying or selling their own currency on the spot market to influence the exchange rate at sizes no commercial participant can match

- Forward guidance — public statements and policy signals that traders price into the market through speculative positioning

- Currency reserve management — accumulating or liquidating foreign currency reserves as part of broader monetary strategy

The Federal Reserve, European Central Bank, Bank of Japan, Bank of England, and their counterparts globally are the institutions whose decisions create the fundamental conditions that all downstream forex activity operates within. Their direct interventions are infrequent but significant. The rest of the time, their influence is indirect — transmitted through interest rate differentials, inflation expectations, and monetary policy communications.

2. Tier 1 Commercial and Investment Banks — The Interbank Market

Below central banks sits the interbank market — a continuous, decentralised network where the world’s largest commercial and investment banks trade currencies directly with each other.

Key Interbank Market Facts

- Tier 1 participants include JPMorgan Chase, Citigroup, Deutsche Bank, UBS, Barclays, HSBC, Goldman Sachs, and Morgan Stanley

- Transactions happen at sizes of hundreds of millions to billions of dollars per trade

- Interbank rates form the reference point from which all downstream prices are derived

- This is where true price discovery happens in the OTC forex market

The interbank market is inaccessible to retail participants and to most retail brokerages directly. Access requires prime broker relationships — typically with Tier 1 banks — that extend credit lines, provide connectivity to interbank pricing, and handle post-trade clearing and settlement. These relationships form the foundation of a brokerage’s liquidity infrastructure, and the terms on which they are obtained significantly affect the trading conditions the brokerage can offer downstream.

3. Sovereign Wealth Funds and Institutional Asset Managers

Sovereign wealth funds — state-owned investment funds managing national savings accumulated from oil revenues, trade surpluses, or other sources — are among the largest forex market participants by assets under management.

Examples of Major Sovereign Wealth Funds

- Abu Dhabi Investment Authority (ADIA)

- Norway’s Government Pension Fund Global

- China Investment Corporation (CIC)

- Kuwait Investment Authority (KIA)

When these funds rebalance portfolios or make cross-border acquisitions, the resulting currency flows can be large enough to move exchange rates over extended periods — particularly in less liquid currency pairs. Institutional asset managers — pension funds, mutual funds, insurance companies — similarly generate sustained forex demand through international investment activity, hedging programs, and currency overlay strategies.

4. Prime Brokers and Prime of Prime Providers

Prime brokers occupy a critical infrastructure role between the interbank market and the broader ecosystem of retail brokerages and trading firms.

What Prime Brokers Provide

- Credit facilities — extending leverage to institutional clients

- Liquidity access — direct connectivity to interbank pricing

- Price aggregation — consolidating feeds from multiple Tier 1 sources

- Clearing and settlement — handling post-trade processing at institutional scale

For retail brokerages, direct prime broker relationships have historically required trading volumes that many operations cannot meet. This created the Prime of Prime model — specialist intermediary providers that aggregate access from one or more prime brokers and offer it downstream to retail brokers at lower volume thresholds and more flexible credit terms.

The quality of the Prime of Prime relationship — in terms of spread depth, fill rates, credit terms, and uptime reliability — has a direct and measurable effect on the execution quality a brokerage can offer its clients.

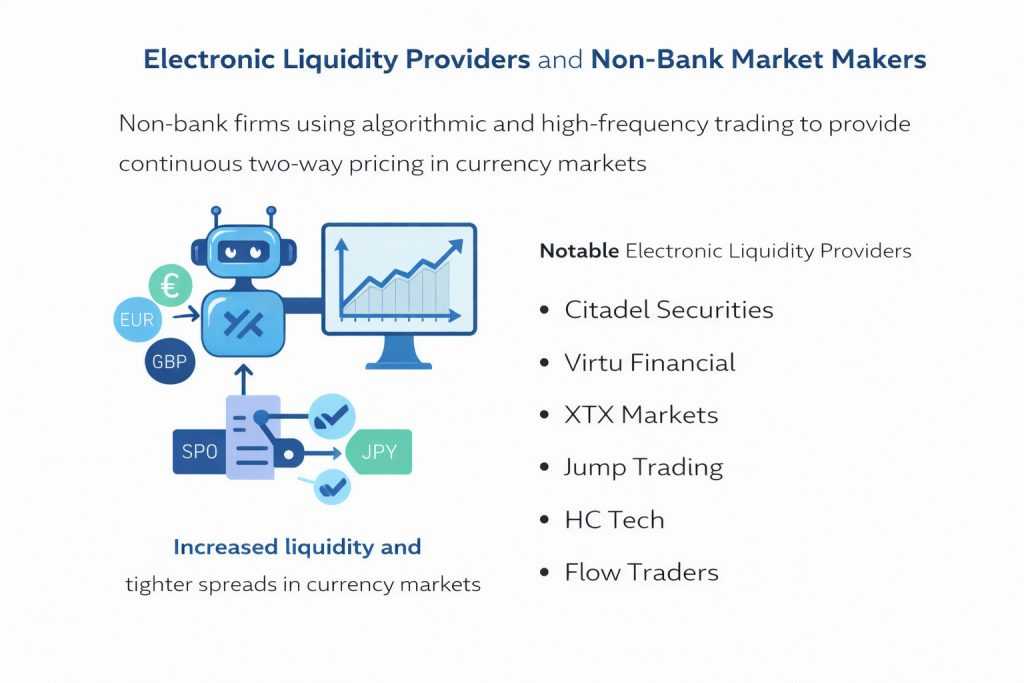

5. Electronic Liquidity Providers and Non-Bank Market Makers

A significant and growing category of forex market participants are Electronic Liquidity Providers (ELPs) — specialised non-bank firms that use algorithmic trading and high-frequency trading infrastructure to continuously quote two-way prices across currency pairs.

Notable Electronic Liquidity Providers

- Citadel Securities

- Virtu Financial

- XTX Markets

- Jump Trading

- HC Tech

- Flow Traders

ELPs compete with Tier 1 banks on spread and execution quality. Their presence has generally contributed to tighter spreads and better fill rates across the market — including in the feeds that eventually reach retail participants. Their role in the liquidity stack has increased significantly since the 2008 financial crisis, as regulatory capital requirements reduced bank appetite for market-making activity.

6. Liquidity Aggregators

Liquidity aggregators occupy the critical infrastructure layer that sits between liquidity providers and retail brokerages. Their function is to consolidate real-time price feeds from multiple sources — prime brokers, Tier 1 banks, ECNs, electronic liquidity providers — into a single composite best-bid-offer.

What Liquidity Aggregation Enables

- Smart order routing — automatically directing orders to the best available venue at execution time

- Competitive pricing — combining multiple sources ensures the tightest possible spread

- Redundancy — multiple liquidity connections reduce single-point-of-failure risk

- Scalability — one aggregated feed serves the full client base without per-source management overhead

Without aggregation, a brokerage would need to manage connectivity to each liquidity source separately, monitor prices across all feeds simultaneously, and route orders manually. Aggregation automates this process, enabling retail brokers to offer institutional-grade pricing without institutional-scale infrastructure. The commercial and operational implications of how forex aggregation works are laid out in detail here.

7. Hedge Funds and Proprietary Trading Firms

Hedge funds are among the most active speculative participants in the forex market. Unlike multinational corporations that exchange currencies to facilitate trade, hedge funds trade currencies primarily for profit.

Common Hedge Fund Forex Strategies

- Directional macro trading — taking large positions on expected currency movements based on economic analysis

- Carry trade — borrowing in low-interest-rate currencies and investing in high-yield currencies

- Statistical arbitrage — exploiting pricing discrepancies across currency pairs or venues

- Trend following — systematic strategies that follow established exchange rate trends

Large macro hedge funds can accumulate positions large enough to exert meaningful pressure on exchange rates, particularly during periods of low liquidity. Proprietary trading firms — including the prop firm model where retail traders operate with firm capital — represent a further layer of speculative participation that has grown substantially since 2020.

8. Retail Forex Brokers

Retail forex brokers are the participant category most traders interact with directly. They sit between the institutional liquidity infrastructure above them and the retail market below, providing individual traders with access to currency markets through trading platforms.

What Retail Brokers Manage

- Trading platform provision and maintenance

- Client onboarding and KYC verification

- Deposit and withdrawal processing

- Customer support operations

- Risk management and exposure monitoring

- Regulatory compliance and reporting

- IB and affiliate program management

Retail Broker Execution Models

| Model | Order Handling | Revenue Source | Conflict of Interest |

|---|---|---|---|

| STP / ECN | Routed to liquidity providers | Spread markup + commission | None |

| Market Maker | Internalised (B-Book) | Spread + client losses | Yes |

| Hybrid | Profiling-based routing | Both | Partial |

The full operational scope of what a retail forex brokerage involves — and what it takes to build and run one at scale — is examined in depth in this guide.

9. Multinational Corporations

Multinational corporations (MNCs) participate in the forex market not for speculative profit but to facilitate their core business operations and manage currency risk.

Why MNCs Participate in Forex

- Trade settlement — exchanging currencies to pay suppliers or receive payment in foreign markets

- Currency hedging — using forwards, options, and swaps to protect against adverse exchange rate movements

- Cross-border M&A — large acquisitions generate concentrated currency demand that can move rates

- Treasury management — managing ongoing FX exposure across multiple operating currencies

Corporate forex activity generates the underlying economic demand for currencies that drives long-term exchange rate trends — distinct from the speculative flows that drive short-term volatility.

10. Retail Traders

Retail traders represent the largest participant category by number but the smallest by individual transaction size. They access the market through retail brokers, trading in sizes ranging from micro lots to standard lots, typically using leverage to control positions larger than their account equity.

Retail Trader Characteristics

- Trade through online brokers with leverage

- Account sizes from a few hundred to tens of thousands of dollars

- Motivated by speculation, hedging, or income generation

- Collectively contribute to overall market volume and liquidity

- Limited individual price-forming impact compared to institutional participants

The growth of retail forex participation over the past two decades has been driven by platform accessibility, leverage availability, and the proliferation of online brokerages offering increasingly competitive trading conditions.

11. Regulators and Regulatory Bodies

Regulators define the operating environment for all commercial participants. Their requirements vary significantly by jurisdiction.

Key Global Forex Regulators

| Regulator | Jurisdiction | Key Focus |

|---|---|---|

| FCA | United Kingdom | Client fund segregation, leverage limits |

| ASIC | Australia | Retail client protections, capital requirements |

| CySEC | Cyprus / EU | MiFID II compliance, reporting |

| ESMA | European Union | Cross-border regulatory standards |

| CFTC / NFA | United States | Leverage restrictions, registration |

| MAS | Singapore | Institutional and retail oversight |

The choice of licensing jurisdiction is one of the most commercially consequential decisions a new brokerage makes — affecting capital requirements, permissible leverage levels, client onboarding processes, and the markets accessible to clients in different geographies.

How These Participants Connect

The forex market functions because these participant categories are connected through interlocking commercial relationships and technical integrations.

The Forex Market Infrastructure Chain

- Central banks set monetary policy → feeds into interbank pricing

- Tier 1 banks trade with each other → establish benchmark exchange rates

- Prime brokers aggregate interbank access → extend it to institutional clients

- Liquidity aggregators consolidate feeds → deliver composite best-bid-offer to brokers

- Retail brokers present pricing to traders → handle execution, clearing, compliance

- Traders place orders → flow back through the same infrastructure in reverse

At every layer, each participant adds something — credit, technology, aggregation, distribution, compliance, client service — and extracts value in return. The efficiency of this chain, and the quality of the relationships and infrastructure at each level, ultimately determines what trading conditions look like at the retail end.

For anyone building a brokerage, evaluating a liquidity setup, or simply trying to understand where the price on a trading screen actually comes from — this is the infrastructure that produces it.

Request a Consultation on Building Forex Market Infrastructure

Get expert guidance on how to structure your brokerage within the broader forex market ecosystem. We’ll help you evaluate liquidity access, aggregation models, prime relationships, regulatory positioning, and operational architecture before you scale.

Together, we’ll review your business objectives and outline an infrastructure strategy aligned with institutional-grade standards and long-term sustainability.